- FirstService Residential Welcomes Bishop’s Landing Community Association to its Southern Delaware Portfolio

- CleanCapital Secures $145 Million And Acquires 22.7 MW Portfolio From KSI

- Infosys turns to Google Cloud to expand AI portfolio

- Lazard Emerging Markets Core Equity Portfolio Q3 2024 Commentary (Mutual Fund:ECEOX)

- Ready to Boost Your Portfolio? Check Out These 5 Best Altcoins to Invest in For Short-Term Gains

DuPont de Nemours, Inc. (DD – Free Report) benefits from its innovation-driven investment, productivity actions and the acquisitions of the Spectrum Plastics Group and Donatelle Plastics amid headwinds from weaker demand in specific businesses.

Bạn đang xem: Here’s Why You Should Retain DuPont Stock in Your Portfolio – January 10, 2025

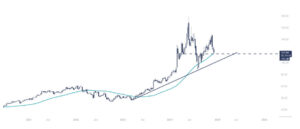

DD’s shares are down 2.3% in a year compared with the Zacks Chemicals Diversified industry’s 12.3% decline.

Image Source: Zacks Investment Research

Let’s find out why DD stock is worth retaining at the moment.

DuPont Gains on Productivity, Innovation & Acquisition

Xem thêm : How Dividend Investors Should Position Their Portfolios For 2025

DuPont remains focused on driving growth through innovation and new product development. Its innovation-driven investment is focused on several high-growth areas. DD remains committed to driving returns from its R&D investment.

The company, in August 2023, completed the buyout of a leading manufacturer of specialty medical devices and components, Spectrum Plastics Group, from AEA Investors for $1.75 billion. The acquisition strengthened DuPont’s existing position in stable and fast-growing healthcare end markets. It is also in sync with its focus on high-growth, customer-driven innovation for the healthcare market.

The buyout of Donatelle Plastics also enhances DD’s exposure in healthcare, expanding its expertise in the medical device market segments. The acquisition introduces complementary advanced technologies and capabilities, such as medical device injection molding, liquid silicone rubber processing, precision machining, device assembly and tool building.

DuPont is also benefiting from cost synergy savings and productivity improvement actions. The benefits of its structural cost actions are expected to be realized in 2024. DD also continues to implement strategic price increases in the wake of cost inflation. These actions are likely to support its results. DuPont is also executing additional restructuring actions and expects annualized cost savings of $150 million from these measures.

DuPont, in May 2024, announced a strategic plan to separate into three distinct, publicly traded companies to unlock value for shareholders and enhance operational focus. The proposed separations of the Electronics and Water businesses will be executed in a tax-free manner for DuPont shareholders, resulting in New DuPont, Electronics and Water as independent entities. Each company will benefit from increased agility and focus within their respective industries while maintaining strong balance sheets and attractive financial profiles. All three resulting companies are anticipated to have strong balance sheets and sufficient capitalization to pursue future growth opportunities.

Softness in Specific Businesses a Concern for DD Stock

DuPont faces headwinds from demand weakness in certain businesses. The Industrial Solutions business is exposed to volume pressure within the Kalrez business. Organic sales in Industrial Solutions declined year over year in the third quarter due to lower volumes. Headwinds from de-stocking in the Kalrez business are expected to continue in the fourth quarter. While DuPont is seeing a recovery lately, additional volume pressure within its industrial-based businesses is expected to continue in the fourth quarter.

Xem thêm : Active ETFs will transform model portfolios, says BlackRock CFO

DD is also seeing lower sales in safety solutions. Organic sales in this business were down by mid-single digits in the third quarter on lower prices and volumes. The business saw lower volumes due to declines in Tyvek medical packaging. The shelter solutions business is also facing headwinds in North American residential construction markets, which is impacting sales. Despite a recovery, volume pressure in these businesses is likely to continue in the fourth quarter.

DD’s Zacks Rank & Key Picks

DD currently carries a Zacks Rank #3 (Hold).

Better-ranked stocks in the Basic Materials space are Carpenter Technology Corporation (CRS – Free Report) , ICL Group Ltd (ICL – Free Report) and ATI Inc. (ATI – Free Report) . While CRS sports a Zacks Rank #1 (Strong Buy), both ICL and ATI carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Carpenter Technology beat the Zacks Consensus Estimate in each of the last four quarters, with the average earnings surprise being 14.1%. CRS’ shares have soared 174% in the past year.

The Zacks Consensus Estimate for ICL Group’s current-year earnings has increased by 2.9% in the past 60 days. ICL beat the consensus estimate in each of the last four quarters with the average surprise being 18.1%.

ATI beat the consensus estimate in three of the last four quarters while missing once. In this time frame, it has delivered an earnings surprise of roughly 3.7%, on average. ATI has gained around 30% in the past year.

Nguồn: https://earnestmoney.skin

Danh mục: News